![CBF2D5DD-379E-4240-B922-9B02697B7958-2.png]](https://kb.smooth.tech/hs-fs/hubfs/CBF2D5DD-379E-4240-B922-9B02697B7958-2.png?height=50&name=CBF2D5DD-379E-4240-B922-9B02697B7958-2.png)

What is a Chargeback?

A chargeback is a reversal of a credit card payment initiated by the cardholder's issuing bank. It can be a significant cost to businesses, both in terms of lost revenue and additional fees. Understanding the difference between legitimate and illegitimate chargebacks is key to effectively managing them.

Types of Chargebacks

- Legitimate Chargebacks: Occur due to reasons like unrecognized transactions by the cardholder, non-delivery of goods, or transaction errors.

- Illegitimate Chargebacks (Friendly Fraud): Arise when a cardholder unjustly disputes a transaction to avoid payment.

Preventative Measures

To minimize the occurrence of chargebacks, consider the following strategies:

- Use clear and detailed product descriptions to avoid misunderstandings.

- Maintain transparent communication about your refund and return policies.

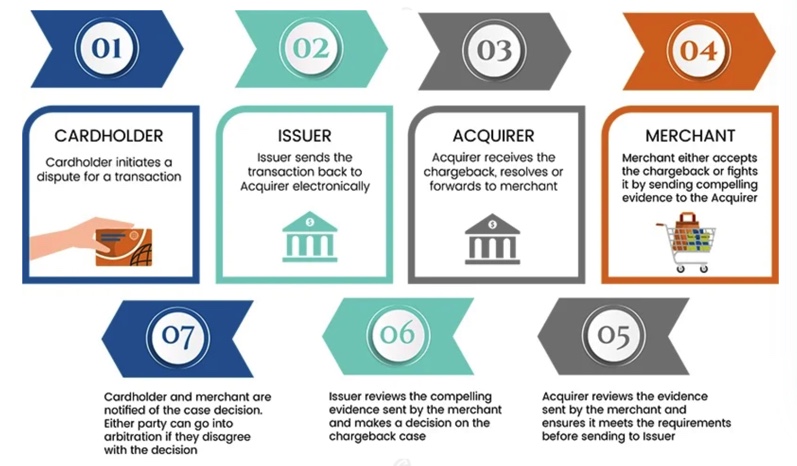

The Chargeback Process

- Initiation: A cardholder disputes a transaction, and the issuing bank initiates a chargeback.

- Notification: The merchant is notified and can either accept the chargeback or dispute it.

- Dispute: If disputed, the merchant submits evidence to counter the chargeback claim.

- Resolution: The issuing bank reviews the evidence and makes a final decision.

Chargeback Reason Codes

Chargeback reason codes are categorized by card networks like VISA, MasterCard, and American Express. Each code identifies a specific reason for the chargeback, such as unauthorized transactions or processing errors. Familiarity with these codes is crucial for effective dispute resolution.

For a full list of Chargeback Reason Codes, Click Here.

Smooth Commerce’s Role in Chargeback Management

Smooth Commerce provides robust support to clients facing chargebacks, including:

- Identity validation measures during customer registration.

- Verification of credit card details to prevent unauthorized transactions.

Disputing a Chargeback

Merchants have the right to dispute chargebacks. The dispute process involves providing evidence that a transaction was legitimate and complied with all required protocols. Disputing a chargeback can be a detailed process, but it's essential for protecting your business from unwarranted losses. Here’s a step-by-step guide to effectively dispute a chargeback:

1. Understand the Chargeback Reason

- Each chargeback comes with a specific reason code. Understand this code as it dictates the type of evidence you’ll need to provide.

2. Gather Relevant Documentation

- Collect all pertinent information related to the transaction. This can include:

- Signed receipts or invoices.

- Proof of delivery (tracking numbers, delivery confirmation).

- Correspondence with the customer.

- Transaction records showing the card was present, if applicable.

- Proof of the customer’s history of purchases (if a repeat customer).

- Documentation showing that the product or service was as described.

3. Prepare a Compelling Response

- Draft a response that clearly addresses the reason for the chargeback. Include all relevant evidence that supports your case. Be concise, but thorough.

4. Understand Time Limits

- Time is crucial in chargeback disputes. Be aware of the deadlines for submitting your evidence, which vary depending on the card network (Visa, MasterCard, etc.).

5. Submit Your Dispute

- Send your dispute through the proper channels. This is usually done through your payment processor or the bank that processes your transactions.

6. Monitor the Dispute Process

- Stay on top of the dispute once submitted. Be prepared to provide additional information if requested by the bank or card network.

7. Learn from the Outcome

- Regardless of the outcome, use the experience as a learning opportunity to prevent future chargebacks. Analyze what led to the dispute and how your internal processes could be improved.

Frequently Asked Questions

-

What is the difference between a chargeback and a refund?

- A refund is a voluntary transaction reversal by the merchant, while a chargeback is initiated by the cardholder through their bank.

-

How can merchants reduce the risk of chargebacks?

- By implementing fraud detection tools, clear communication about policies, and meticulous record-keeping.

-

What are some common reasons for chargebacks?

- Unauthorized transactions, errors in processing, and dissatisfaction with goods or services are common reasons.

Reference Your Payment Processor for Detailed Chargeback Information

While this guide offers a comprehensive overview of chargebacks, the specifics can vary depending on your payment processor. For detailed information tailored to your payment processing system, we strongly recommend referring to the resources provided by your payment processor. This can include specific procedures, documentation requirements, and timelines for handling chargebacks.

Moneris

For merchants using Moneris, you can find in-depth information about chargebacks, including how to understand and respond to them, at the following link: Moneris Chargeback 101. This resource provides valuable insights specific to the Moneris system, helping you navigate the chargeback process more effectively.

Worldline/Bambora

For those using Worldline/Bambora as your payment processor, detailed guidance on handling disputes can be found here: Worldline/Bambora Disputes. This section covers the essentials of managing chargebacks within the Worldline/Bambora system, offering step-by-step guidance and tips for successful dispute resolution.

Why Refer to Your Payment Processor?

Each payment processor has its unique set of rules and procedures for handling chargebacks. By referring to these specific resources, you can:

- Understand the exact process and requirements for disputing chargebacks with your processor.

- Access processor-specific forms and documentation guidelines.

- Stay updated with any changes in the chargeback policies of your payment processor.

Navigating the world of chargebacks can be complex, but your payment processor is a vital resource in this journey. We encourage you to utilize these specific resources from Moneris and Worldline/Bambora for the most accurate and relevant information pertaining to your chargeback disputes.

Conclusion

Understanding and managing chargebacks is a vital aspect of modern business operations. By adopting proactive measures and staying informed, merchants can significantly reduce the impact of chargebacks on their businesses.